Take Control of Your Future

Loans for Self-Managed Super Funds (SMSF Loans)

The retirement stereotypes of days spent on the golf course or walking along golden beaches, whilst still true for some, are no longer the norm. Travelling around Australia or overseas, taking care of grandchildren, undertaking further education, doing volunteer work, and even starting a new business or working part time are all common in modern retirement.

Whatever your retirement plans are, you want to be comfortable and worry-free. Your superannuation is one of the most important, not to mention tax efficient ways to save for this rewarding stage of your life. Unfortunately, almost half of Australians aged between 45 and 64 do not feel confident they have adequate funds to do what they want in retirement.

Having the right plans in place to manage and grow your super can make a significant difference to your retirement goals. For some, this includes managing their own super independently through a self-managed superannuation fund (SMSF).

An SMSF is your own personal super fund that gives you control to make the important decisions around how your super is invested. Managing your own super through an SMSF can be extremely rewarding, but they are not for everyone because they require your close attention and dedication.

Use A Self-Managed Super Fund Loan to:

- Purchase residential and/or commercial investment property

- Refinance an existing SMSF investment property loan

Benefits Of a Self-Managed Super Fund:

Purchase residential and/or commercial investment property – borrow through your SMSF to purchase residential and/or commercial property to be held in a trust for the duration of the loan term.

Protect your fund’s other assets – should the loan fall into default, rights of retrieval are restricted to the secured property (and any additional security provided by the guarantors).

Potential gearing advantages – it may be possible to claim interest and expenses paid on the loan as deductions against rental income for tax purposes.

Pay via rental income, SMSF investments or contributions – income from rent, other SMSF investments and super contributions can all be used to illustrate serviceability and reimburse the loan.

Incorporate with your present SMSF – the loan structure can be setup to easily incorporate with most existing SMSFs.

How Can You Invest In Property With Your SMSF?

Property Investment in Australia has seen its ups and downs over the last couple of decades as investors deal with the rise and fall of property prices, yields, and costs of living. But as investments go, it is still a sound strategy.

Property investment is still regarded as the largest investment an individual can make with their money and is one of the best ways to secure a sufficient retirement income. And the best part is you can borrow using your SMSF to fund the purchase. Gone are the days, where you have to go through the costly and rigorous process that is associated with acquiring a property of your choice.

Now, in Australia, you can save for a rainy day, by setting up a SMSF primarily for property purchase. We can help you fund SMSF Property Loans up to 80%* of a property value. The Fund will then contribute cash to pay the deposit and to meet the legal costs and stamp duty. Your SMSF will also cover the interests, maintenance, insurance, rates, body corporate fees, property management and other expenses incurred during the investment process. The property is held in trust and the legal title is either transferred to the SMSF when the loan has been repaid or the property is sold.

Example Case Study

Joe & Jane Borrower have a SMSF with $150,000 in cash. They would like to buy an investment property within their SMSF. The property is worth $400,000 which means the SMSF doesn’t have enough money to cover the full cost of the purchase. In this case, the SMSF trustees can apply for an SMSF Property Loan.

So how exactly does it work?

The Borrowers will need to ensure that it is appropriate for the SMSF to borrow money to purchase the investment property. They may seek independent financial and legal advice to get confirmation.

Once confirmed, they begin building the trust structures required for the loan, ensuring they comply with the related superannuation laws. The SMSF loan can then be taken out by the SMSF Trustee.

The Borrowers will also need to set up a holding trust, which will function as the legal owner of the property. To purchase the property, the SMSF can use the $150,000 it has accessible in cash and borrow the shortfall ($250,000), using the investment property as security for the loan.

The holding trust then becomes the legal owner of the property, while the SMSF is the beneficial owner and receives the rental income.

Who is permitted to apply?

- An Australian resident with an existing SMSF or

- In the process of establishing an SMSF

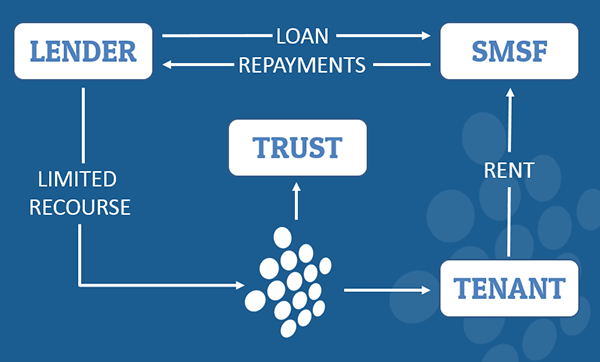

How SMSF Loans workHow SMSF Loans work diagram- A visual example

How SMSF Loans workHow SMSF Loans work diagram- A visual example

Important Note

It is significant to note the loan is a limited recourse loan. In the occasion of a default, the lender has recourse to the security and any additional assets supplied by the guarantor(s). The Lender won’t have recourse to any other assets held in the Borrowers’ SMSF. Once the loan is repaid the legal ownership of the property can be transferred to the Borrowers’ SMSF.

This case study, including all names and details, is a fictitious example and is supplied for illustrative purposes to attest the fundamental outline of how a SMSF loans can be structured. It should not be relied upon for any motive and provides no determination of the possible tax consequences of a SMSF Property Loan. As with any financial investment decision, we urge all of our clients to obtain independent legal, financial and taxation advice.

Why Choose Lifestyle Loans?

With over 20 years of industry leading experience, rest assured your needs are our top priority. We offer SMSF Property Loans from Australia’s leading SMSF lenders and are constantly on the hunt for the most competitive SMSF home loan products available.

Talk to one of our SMSF experts

Call us during business hours on (03) 9663 0009 or send a message to have a chat to our SMSF Finance experts. Did you know you can also get the latest tips and advice by liking us on Facebook or following us on Twitter.